Why Launch our Multifamily Real Estate Fund Now?

CHARLESTON, SC | May 24, 2024

In last week’s email we discussed why we like Southeast workforce multifamily as an asset class. This week we are going to talk about why - despite fundamentally liking the asset class - we had not purchased a property for 18-months, but why we are now launching Sunbelt Multifamily Fund III (“SB3”) with its first acquisition.

We had expected to launch SB3 more than a year ago but were unable to deploy capital because we saw a disconnect between the price where sellers wanted to sell versus where we wanted to buy. Sellers were trying to sell at prices achieved in prior years. However, sponsors like Ballast Rock had to pay higher operating costs and higher debt costs, so 2021 prices no longer made sense. From our experience of underwriting more than 400 deals in the last 18-months, the gap between where we (and the market more broadly) wanted to buy versus where sellers wanted to sell was typically between 15%-25%. We were not alone in this experience and this gulf between buyers and sellers saw a 61% decrease in multifamily transactions in 2023 while multifamily debt origination (so both acquisitions and refinancings) declined 52% year over year in 20231 and in Q1 2024 dropped to their lowest level since 2015.

We felt that patience would be rewarded as multifamily asset prices would fall given the increasing number of motivated sellers suffering higher operating/debt costs and further forced by impending debt maturities to either sell or refinance. Additionally, those looking to refinance in this higher interest rate and more expensive operating environment are being forced to provide additional equity capital given challenging Debt Service Coverage Ratio (“DSCR”) requirements from lenders.

Increasingly Motivated Sellers

We expect expiring rate caps and loan refinancing will be a key driver for multifamily transaction activity over the next 12-18 months. As can be seen in the graph below, a significant number of Multifamily loans are coming due in 2024 and 2025:

We believe this upcoming “maturity debt wall” will present a limited number of relatively attractive buying opportunities, as there will be sponsors who are unable to refinance individual assets on economic terms based on current loan-to-values ("LTVs”) and materially heightened borrowing costs. At the end of 2023, 36% of upcoming securitized multifamily debt maturities had a DSCR of 1.25x, per their most recent financials, compared with only 23% with a DSCR of 2.0x or greater.[1] These maturities will struggle to refinance given their inadequate DSCR ratios, even before taking lender LTV limits (given lowered valuations) into account. These sponsors will need to either renegotiate with their lenders to “extend and pretend,” raise additional capital from their LP investors, or raise expensive rescue capital.

“Extend and pretend” is a playbook familiar to lenders from the 2008 Great Recession. We have already seen this strategy being used by borrowers in the current cycle: according to data from the Mortgage Bankers Association, 37% of Commercial Real Estate Loans that were set to mature in 2023 were extended to 2024. However, the ability to continue extending loans has a limit, so if borrowers cannot raise additional capital, a very real prospect for failing sponsors, the only other viable option is to sell the underlying asset.

Falling Multifamily Prices

A property’s cap rate is its net operating income divided by its price. So, all things being equal, lower cap rates generally mean a higher price for an asset and vice versa. As can be seen in the graph below, which shows cap rates for different real estate sectors going back to 2005, cap rates had been on a steady march lower (i.e. prices were going up) since the aftermath of the financial crisis.

Average multifamily cap rates went from a peak of 8% after the 2008 Financial Crisis, to around 4.25% in 2022. But since the Fed started raising rates, average multifamily cap rates have gradually increased to 5.8%. That represents a fall in price (assuming no change in net operating income) of almost 27% from the recent peak. While we cannot say with certainty that prices will not continue to fall lower, given the fall in prices we have seen in the last 18-months, we believe current levels do offer an attractive entry point once again, particularly considering SB3’s target hold period.

Multifamily Sector Fundamentals

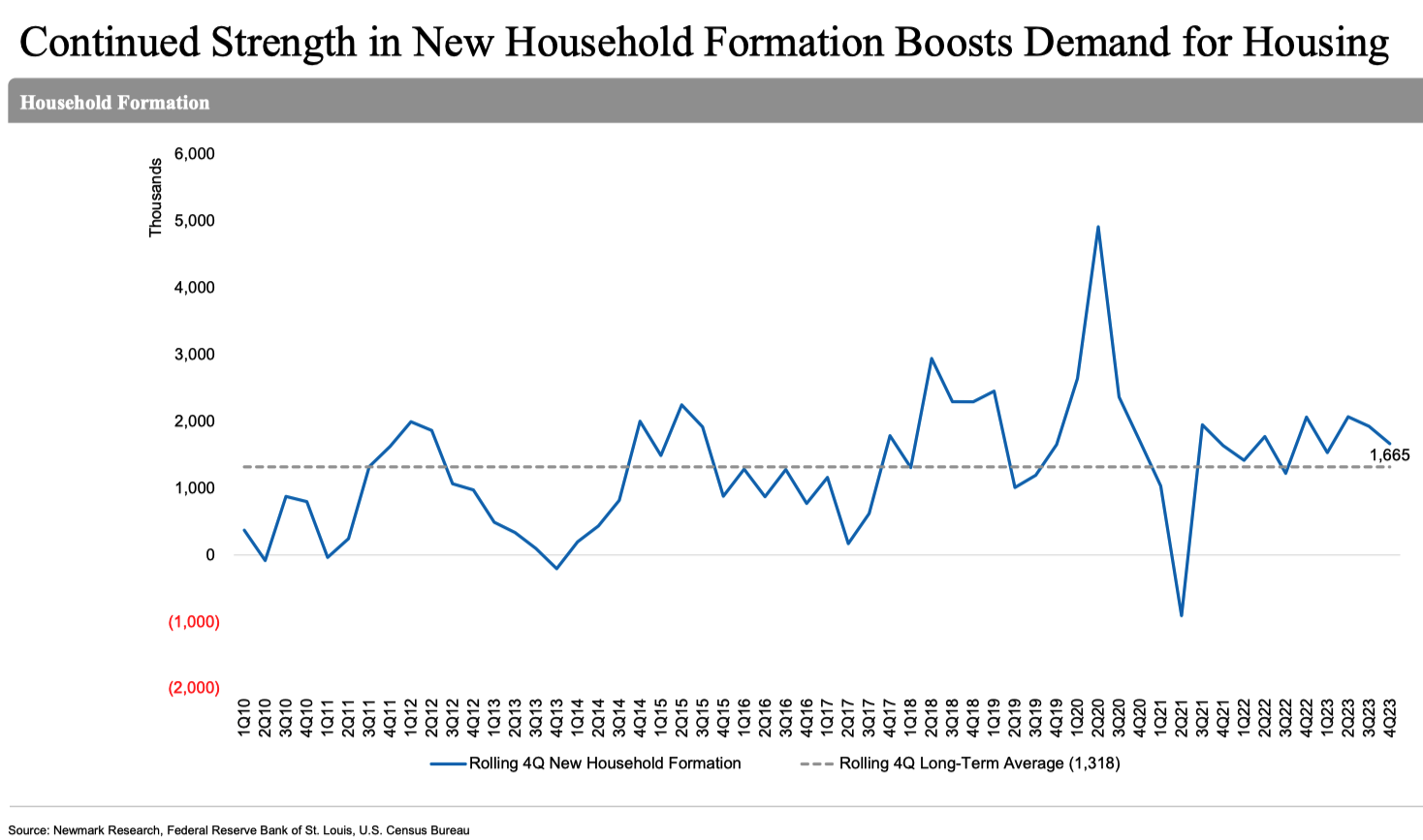

However, it is not all doom and gloom for the sector, in fact the multifamily demand and supply fundamentals remain attractive both from the demand perspective as new household formations were running 47.0% higher than the 10-year average in Q4 2023,[1] and given the heightened cost of capital from early 2022 onwards and the construction cycle, the supply of multifamily units nationally will drop off significantly after the surge of multifamily unit deliveries in 2024.

Renting vs. Home Ownership

Meanwhile it remains cheaper than ever to rent relative to buying a home. Increasing 18.4% year over year, the spread between homeownership and rental costs grew to $824 in the first quarter of 2024.[1] Driven by record-level interest rates, renting continues to be significantly more economical than owning a home.

Additionally, debt capital markets remain wide open to borrowers, particularly given the Government Sponsored Enterprise (“GSE”) lenders mandated support (e.g. Fannie, Freddie, and HUD). GSE participation in the multifamily sector debt capital markets have increased from 40% in 2021 and 2022 to 54% in 2023,[1] mainly stepping into the shoes of banks and CMBS.

While we expect to see an uptick in transaction volumes driven by more motivated sellers, we do not expect multifamily in the Southeast to experience the same distress currently being seen in areas like the office sector and think buying opportunities are likely to be limited. This is because, unlike office space, there has not been a structural change in how people are using multifamily – people still need safe, comfortable, and affordable housing.

We launched SB3 because we found a specific asset that fits our strict quantitative and qualitative targets, but also because we expect to see some multifamily prices adjustment over the short- to medium-term. However, this potential market opportunity has led to significant interest from investors, and transaction volumes in early 2024 are still subdued, so acquiring assets is still a highly competitive process (e.g., we have underwritten over 400 deals to acquire this first asset for the fund).

Ultimately, we believe our patience has paid off and, while there is still a lot of uncertainty about the path ahead for interest rates and property prices, we are excited about launching the fund by acquiring the first property that met our underwriting standards in more than 18-months.

[1] Newmark 4Q2023 and 1Q2024 United States Multifamily Capital Markets Reports

Prior Sunbelt Multifamily Funds

Ballast Rock launched Sunbelt Multifamily Fund I (“SB1”) in 2019 and between February 2019 and January 2021 acquired nine properties totaling 1,110 apartment units for $63,630,000. SB1 began dispositions in early 2022, generating gross proceeds of $60,450,000 from the first four properties sold. The 593 apartment units involved were acquired at an average cost of $53,583 per unit and sold at an average cost of $101,939 per unit. Ballast Rock anticipates exiting the remaining five assets in SB1 opportunistically over the next 12 to 18 months.

Sunbelt Multifamily Fund II (“SB2”), launched in 2021 and between February 2021 and January 2023 acquired nine properties totaling $101,408,000, with 1,039 apartment units.

In April of 2023 Ballast Rock launched Ballast Rock Capital, its broker-dealer. Ballast Rock Capital is a member of the Financial Regulatory Authority (FINRA) and the Securities Investor Protection Corporation (SIPC) and is registered with the Securities and Exchange Commission (SEC).

About Ballast Rock Group

Ballast Rock Group is an integrated investment management company specializing in delivering risk-adjusted returns, accurate, and timely advice, high quality frequent reporting, and direct access to management. Ballast Rock Group operates Ballast Rock Asset Management, Ballast Rock Private Wealth, and Ballast Rock Capital. Ballast Rock Asset Management comprises Ballast Rock Real Estate, which includes the firm’s Sunbelt multifamily real estate funds, and Ballast Rock Ventures, comprising venture capital and private equity teams. Ballast Rock Private Wealth is a registered investment advisor, with a focus on alternative strategies. Ballast Rock Capital is awaiting approval to become a FINRA-registered broker-dealer. Ballast Rock is committed to being a driver of positive change. The diversity of our team members brings valuable new perspectives to our industry for the benefit of our stakeholders and the broader community.

Insights Article Disclaimer

This article is an opinion piece written by a multifamily sponsor and truncated to focus on what the author believes are the key relevant data points and should not be relied on as a complete real estate market overview. Data and graphs were borrowed from various sources including Newmark’s 1Q2024 and 4Q2023 Unites States Multifamily Capital Markets Reports which will provide a broader market view point.

Investment Disclosure

The information contained above has been prepared by Ballast Rock Holdings LLC (“Ballast Rock”) without reference to any particular reader’s investment requirements or financial situation. Past returns are no guide to future performance. Potential investors are encouraged to consult with professional tax, legal, and financial advisors before making any investment into a private offering of securities. An investment in private securities would be speculative and would involve a high degree of risk. Investors must be prepared to bear the economic risk of such an investment for an indefinite period of time and be able to withstand a total loss of their investment. Please carefully consider the investment objectives, risks, transaction costs, and other expenses related to an investment prior to deciding to invest. Ballast Rock Capital LLC (“BRC”), MEMBER: FINRA / SIPC. BRC’s registered head office is 460 King Street, Suite 200, Charleston, SC, 29403. Tel: 800-204-2513. To check background information about BRC and its representatives, visit FINRA’s BrokerCheck. Please see important disclosure information in our Form CRS.