Late Cycle Investing: Read the Data, Not the Headlines!

I recently had the pleasure of presenting to a large group of real estate investors in Dallas at the annual 506 Group Investor Forum. As a participant in a panel about late cycle investing, it was apparent that this subject is top of mind for many investors. Most investors have benefited from a ten-year bull run after the longest uninterrupted economic expansion in U.S. history. Many are now looking across the U.S. economy and globally at frothy prices in many asset classes and questioning how to position themselves and their portfolios for what is to come. In this article we will frame the stages of the business cycle, attempt to ascertain where the U.S. economy is in that cycle, and ultimately discuss things to consider when positioning one’s portfolio for late cycle investing and beyond. (1) I will make the case that though we are “late cycle,” we are not “end cycle.” As such, portfolio positioning should start to contemplate recession resilience, yet not let the hangover of the Great Recession drive us to fear-based investing, in particular when it comes to real estate.

When we refer to the “business cycle” for a given economy, what are we talking about?

Here are the four main phases of the business cycle:

Expansion: The economy grows a healthy 2 to 3%. Stocks enter a bull market.

Peak: The economy grows more than 3%. Inflation sends prices up. There are asset bubbles. The stock market is in a state of "irrational exuberance." Talking heads announce we are in a "new normal." Authors publish books with titles such as "Dow 30,000."

Contraction: Economic growth slows but isn't negative. Stocks enter a bear market.

Trough: The economy contracts, which signals a recession. Economic experts predict it will continue for years.

Phases of the Business Cycle

Source: Fidelity

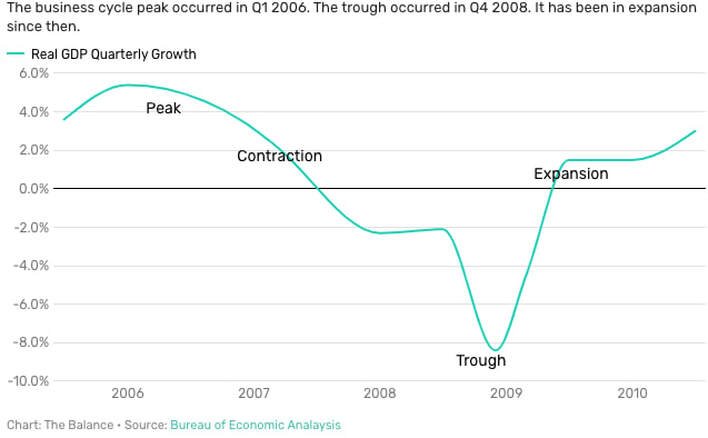

The U.S. economy has been in the expansion phase of the business cycle since the last trough in the fourth quarter of 2008. Given expansion phases have historically lasted approximately five years, many pundits are warning that a recession is just around the corner. The line chart below tracks the rise and fall of Gross Domestic Product (GDP) highlighting the stages of the current business cycle.

U.S. Economy Quarterly GDP

Source: The Balance

While pundits warn against heightened recession risk after such a long period of expansion, many of the typical leading indicators of recessions are not present at this time. Recessions have historically been preceded by troubling levels of inflation, negative surprises in growth data, downward revisions to economists’ growth forecasts, deterioration in sentiment, and tightening in financial conditions, none of which we see at this time. While a case can be made that recession risk is higher now than over the past few years, I would argue that we are a far cry from advising investors to significantly shift their asset allocations. (1) Read the data, not the headlines!

Where does the U.S. economy stand now?

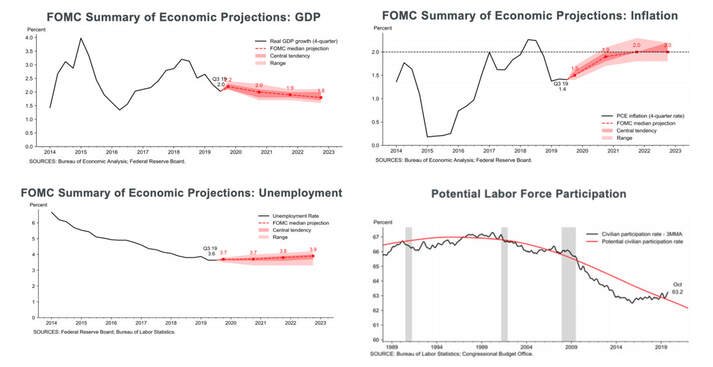

As of now, U.S. data paints a picture of slower growth, but not a looming recession. At the aforementioned real estate forum, Professor John V. Duca, Vice President of the Dallas Federal Reserve Bank, gave an interesting and convincing presentation about how the Fed is currently on track to orchestrate one of the first “soft landings” in U.S. economic history (barring any exogenous event such as a large and expensive global conflict or trade war). The graphs below illustrate how GDP growth is projected to slow, inflation will gradually rise, and unemployment will remain at near full effective unemployment. While each of these indicators represent declines from the current rate of expansion, they paint a picture of a gradual easing into an environment of slower economic growth, rather than an abrupt crash into a recession.

FOMC Key Economic Projections

Source: Dallas Federal Reserve Bank

I am not alone in my view that though the U.S. economy is late in the business cycle, it is not at the end of the cycle, therefore it could be another three to five years before we see negative GDP growth. Wall Street’s fears of an imminent recession are fading too, as proactive Federal Reserve policy, a normalized yield curve, and global economic data signaling a bottoming out of global growth have sparked renewed confidence. (2)

Looking forward, I believe the factors most likely to cause the next recession are trade policy driven by economic nationalism, a geopolitical crisis, and/or a stock market correction driven in part by high levels of corporate leverage. However, it is critical to note that the next recession will be unlike the Great Recession – oversupply and over-leverage in the housing sector are unlikely to cause the next recession – even if housing demand may slow in certain regions.

For those hoping to tactically reposition their portfolios ahead of the next downturn, history suggests that investors wait for clear signs of deterioration in fundamental and price trends before taking defensive steps. However, in certain asset classes (like equities) moves can be extremely rapid and led by institutional investors leaving individual/retail investors to catch a falling sword.

Given historical trends, how should investors position their portfolios for a period of slowing growth?

Investors should focus on investments that offer diversified portfolio access to income generating real estate that features low leverage, low operating risk, and tenants in countercyclical businesses.(1) Timing the market is extremely hard even for professionals, and no investor should think any investment they make is “recession-proof.” That said, low operating risk real estate in high-demand locations lends itself to more consistent performance, thereby generally insulating investors against market downturns. (3)

When one searches for defensive real estate investing, multi-family housing is most often cited, but there are also many commercial tenants that fit the profile of either countercyclical or recession resilient. Certain retail sectors, like auto-parts, tend to be countercyclical (e.g. people extend the life of their cars by buying more parts in a recession rather than buying a new car). Similarly, healthcare also tends to be recession resilient (elective procedures decline, but generally the sector shows little effect from a down cycle). (4)

What asset types/classes should be avoided in a late cycle phase?

High leverage and appreciation-driven assets, where your value/return is primarily based on the sale price of the asset rather than interim cash-flows, can be cause for concern. Examples include: real estate development projects or heavy redevelopment, where project completion and a subsequent sale may be three to five years in the future (i.e. potentially as a recession hits). Investors should also be wary of any asset that is highly reliant on either a future debt re-financing or future equity round to survive. As an example, companies that have not yet reached breakeven are going to struggle as those debt and equity financing markets contract as we get later and later in the cycle.

Conclusion

Despite the fact that I believe this cycle has a lot left to run, consideration of medium-term portfolio positioning is timely for investors with exposure to regions and asset classes more susceptible to recession risk. There are investments better able to weather the volatility of the market than others, such as liability matched net-lease real estate with recession resilient tenants or workforce multi-family real estate, both of which yield immediate and more consistent rental income. Continue to follow and read the data, not just the alarmist headlines. Avoid fear-based decisions and market timing missteps, by steadily and calmly averaging into more defensive investments over the years to come.

At Ballast Rock Capital we help originate and distribute countercyclical and recession resilient real estate funds. Please feel free to connect to learn more about how we work with experienced real estate professionals to offer investors the opportunity to invest in income producing assets with a positive social impact.

-

Please consult your own independent advisor as each investor’s situation is different.

PIMCO Insights: Late Cycle vs. End Cycle

Appreciation and depreciation in real property may be attributable to a number of factors and will be subject to the risks inherent in the ownership and operation of real estate and real estate-related businesses and assets including, without limitation, (i) burdens of ownership of real property; (ii) general and local economic conditions; (iii) changes in supply of and demand for competing properties in an area (as a result for instance of overbuilding); (iv) the resources of tenants; (v) changes in building, environmental and other laws; (vi) energy and supply shortages; (vii) various uninsured or uninsurable risks, natural disasters, changes in government regulations (such as rent control); (viii) changes in real property tax rates; (ix) changes in interest rates; (x) the reduced availability of mortgage funds which may render the sale or refinancing of properties difficult or impracticable; (xi) environmental liabilities; (xii) contingent liabilities on disposition of assets; (xiii) terrorist attacks, war and other factors; (xiv) lack of diversification; (xv) leverage; (xvi) no assurance of investment return; (xvii) illiquid and long-term investment; (xviii) material, non-public information; (xix) no market for interests in the fund; (xx) transfer restrictions; (xxi) investments longer than term; (xxii) inherent uncertainty in projections; (xxiii) risks upon dispositions of the investment; (xxiv) indemnification; (xxv) conflicts of interest; and (xxvi) other activities of management. No risk control mitigant is failsafe.

Forbes: Recession Talk is Growing, is it a Bad Time to Invest in Real Estate