Growth Venture Capital: Navigating a Transforming Investment Landscape

CHARLESTON, SC | February 6, 2025

Author: Simon O’Shea

Chief Investment Officer

Venture capital (VC) is a type of investment that is used to provide funding to startups and early-stage companies with high-growth potential. In contrast to early-stage venture capital funds, which typically invest in Angel, Seed and Series A rounds, growth venture capital invests in more mature startups through Series B or later rounds. While all venture capital investing carries some degree of risk, growth VC typically invests in companies with lower operational risk, more technological maturity, a more fully developed product-market fit, better-defined unit economics, and a better-established customer base.

Emerging from the turbulent market corrections of recent years with renewed strategic potential, we believe that growth-stage venture capital now represents a compelling investment case. We set out the main reasons for our thesis below.

1) Valuation Recalibration

Source: Carta

Like many asset classes, the venture capital landscape of 2020-2021 was characterized by abundant cheap capital which led to inflated valuations. The bursting of the VC “bubble” saw valuations for growth stage (Series B and later) companies fall significantly in 2022 and 2023. The “Series B Valuations in 2024” graph shows median valuations for Series B rounds since Q1 2019; median valuations fell 50%+ between Q1 2022 and Q1 2023 but have now stabilized.

This recalibration of later-stage startup valuations accompanied by a more disciplined approach for deploying capital, offers investors more realistic entry points for high-growth potential, later-stage portfolio companies.

Critically, this valuation reset has not diminished the underlying innovation and potential of technology-driven enterprises. New technologies continue to reshape how we live and work. Instead, increased discipline and capital scarcity has filtered out weaker and more speculative ventures, leaving a more robust cohort of companies with demonstrable market traction, sustainable business models, and clearer paths to profitability or exits.

2) Strong Economic Backdrop and a Rebounding IPO Market

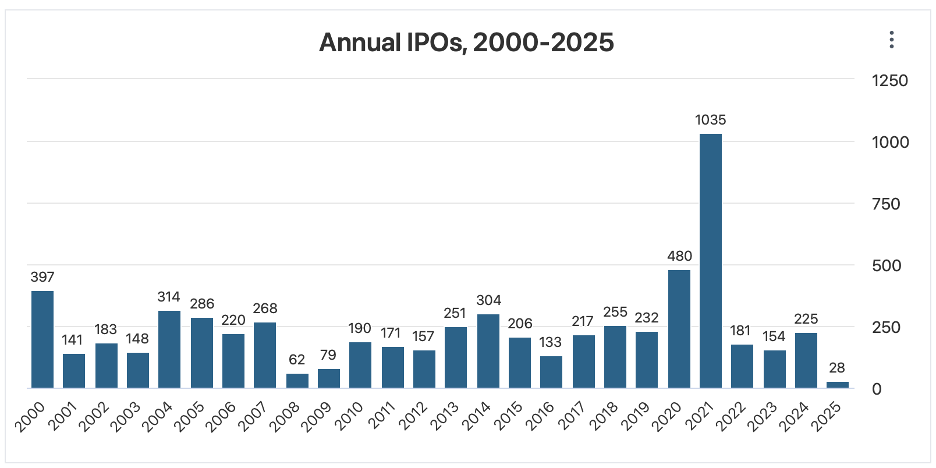

Source: stockanalysis.com

The broader macroeconomic environment has created a favorable investment climate. Interest rates off the highs, combined with a more stable economic outlook, have reduced the opportunity cost of venture capital compared to alternative investments.

Given the correction we have seen in late-stage valuations and the continued elevated levels in public markets, Initial Public Offerings (IPOs) increasingly offer an attractive option for both issuers and investors.

In addition, as can be seen in this 2000-2025 Annual IPOs graph, after a record year in 2021, the number of IPOs in recent years fell dramatically.

As a result, a backlog of mature private companies looking to come to market has developed over the past three years of subdued IPO activity. Many of these companies have reached scale and profitability metrics traditionally associated with public market readiness.

3) Regulatory Environment and Political Landscape

The return of the Trump administration presents a potentially transformative scenario for venture capital funds and their investments. Early indications suggest a relaxation of regulations, including less aggressive implementation of antitrust regulations, simplifying public listing requirements, potentially more favorable tax environment for public offerings, as well as a reduction in complexity and cost of adhering to compliance requirements for emerging companies.

We also expect reduced regulatory barriers for technology companies looking to grow and expand through acquisition which could significantly impact the mergers & acquisitions (M&A) market. A lighter regulatory environment could accelerate M&A interest for growth-stage companies as large incumbents encounter a more permissive landscape for strategic acquisitions.

However, nearly 19% of all primary fundings on Carta in Q2 were reported down-rounds, confirming that valuation expectations are starting to reset lower. It is worth nothing that what is not readily reported are the shadow down-rounds that happen due to liquidation preferences and pay to play rounds.

4) The Impact of the M&A and IPO Markets Reopening

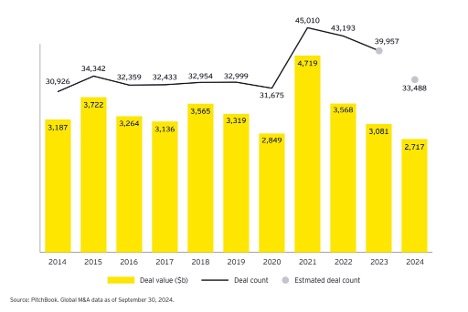

Source: Pitchbook, Global M&A data as of September 30,2024

As has been a common theme, this graph shows M&A activity going back to 2014. It shows 2021 as a record year followed by a significant drop in subsequent volumes and deal values.

The fall in M&A and IPO activity over the last few years led to capital scarcity as fund liquidity has been locked up in portfolio company investments for longer. However, the strong performance in U.S. public equity markets is supportive for growth stage VC valuations as well as giving strategic acquirers more firepower and flexibility to acquire bolt-on acquisitions.

With this expected increase in M&A and IPO activity, older VC funds will realize returns as they exit their historic investments, which will be good for the startup ecosystem as this fresh liquidity to VC funds and distributions to their LP investors, can then be recycled to be deployed into new portfolio company investments.

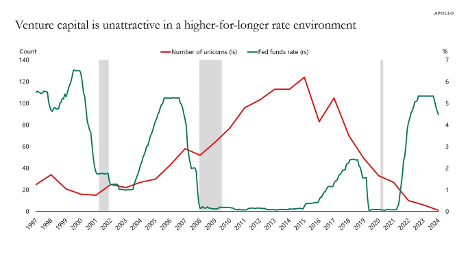

Source: Apollo Asset Management

Risks

While we expect enhanced opportunities for portfolio company exits and strategic positioning to capitalize on deregulatory trends more broadly it is important to note that there are still risks to VC investing.

The most immediate risk is the rate environment. As can be seen in this related graph, the creation of unicorn startups, private companies valued at $1 billion or more, has historically been correlated with the Fed Funds rate to some degree.

But not every portfolio company ultimately becomes a unicorn. In fact, most private company exits occur through an M&A transaction at a valuation of $500 million or below. As such, we believe there are still opportunities to deploy capital, even in a higher rate environment.

Beyond higher rates, uncertainty around potentially escalating global trade wars, stubbornly persistent inflation, and ready access to a highly skilled and qualified workforce in the US are other potential risks to any upside scenarios.

In addition, the Artificial Intelligence (AI) sector has been the largest recipient of VC dollars invested over the last two years. DeepSeek recently showcased its latest AI models, which it says are on a par or better than industry-leading models in the United States at a fraction of the cost. At this time, it is unclear what the long-term impact of this announcement will be – it is potentially negative for those companies who have already spent billions developing their own large language models, but it is likely positive for companies developing AI applications, as it will now likely be cheaper to develop these apps.

To capitalize on the potential opportunities while navigating the risks, fund managers must be disciplined, remain committed to comprehensive due diligence before investing, and focus on portfolio companies with strong management teams, a clear path to profitability, and sustainable competitive advantages. By embracing a more disciplined, data-driven investment philosophy, growth VC funds can capitalize on a market that rewards strategic insight, technological understanding, and measured risk assessment.

About Ballast Rock Group

Ballast Rock Group is an integrated investment management company specializing in delivering risk-adjusted returns, accurate, and timely advice, high quality frequent reporting, and direct access to management. Ballast Rock Group operates Ballast Rock Asset Management, Ballast Rock Private Wealth, and Ballast Rock Capital. Ballast Rock Asset Management comprises Ballast Rock Real Estate, which includes the firm’s Sunbelt multifamily real estate funds, and Ballast Rock Ventures, comprising venture capital and private equity teams. Ballast Rock Private Wealth is a registered investment advisor, with a focus on alternative strategies. Ballast Rock Capital is awaiting approval to become a FINRA-registered broker-dealer. Ballast Rock is committed to being a driver of positive change. The diversity of our team members brings valuable new perspectives to our industry for the benefit of our stakeholders and the broader community.

Investment Disclosure

The information contained in this press release has been prepared by Ballast Rock Holdings LLC (“Ballast Rock”) without reference to any particular reader’s investment requirements or financial situation. Potential investors are encouraged to consult with professional tax, legal, and financial advisors before making any investment into a private offering of securities. An investment in private securities would be speculative and would involve a high degree of risk. Investors must be prepared to bear the economic risk of such an investment for an indefinite period of time and be able to withstand a total loss of their investment. Please carefully consider the investment objectives, risks, transaction costs, and other expenses related to an investment prior to deciding to invest. Ballast Rock Capital LLC (“BRC”), MEMBER: FINRA / SIPC. BRC’s registered head office is 460 King Street, Suite 200, Charleston, SC, 29403. Tel: 800-204-2513. To check background information about BRC and its representatives, visit FINRA’s BrokerCheck. Please see important disclosure information in our Form CRS.